Overview

Key Discussion Points

- Market returns were generally negative over the quarter due to rising rates and inflation and the war in Ukraine. Fixed Income returns were negative, with global bonds underperforming NZ bonds. Alternatives and inflation protecting real assets performed comparatively strongly.

- The model portfolios were well ahead of the peer group for the quarter, extending the lead over 1, 3 and 5 –year horizons.

- For lower risk profiles the alternative allocations and short duration tilt is the main reason for this out-performance, while alternatives have also benefited the higher risk profiles along with the relatively large allocation to real assets.

- NZ bonds are now approaching our estimated fair value when we would start to reduce the large underweight to benchmark duration fixed income. Global bonds are further from our fair value estimates and so we do not propose changing our short duration positioning yet.

- The majority of funds on the APL continue to perform well, with the only two funds on watch: Dimensional 2-Yr Fixed Interest due to poor peer-relative returns and Kernel Global Infrastructure due to their short history.

- As part of our ongoing commitment to assessing the impact of climate risk in your portfolio we have provided a summary of the funds with a low-carbon focus in your portfolio and extended our greenhouse gas emissions analysis across the total growth exposure (shares, property, and infrastructure). This analysis shows a material reduction in the greenhouse gas emissions of your portfolio versus a benchmark.

Recommendations

- Consider reducing the tilt to NZ cash enhanced funds vs. NZ bonds by a third.

- Replace iShares EM Equity Fund and Dimensional EM Value Trust with Dimensional EM Sustainability Trust.

Financial Market Update

Only Global Listed infrastructure (and cash) positive for the quarter

Market Commentary

From inflation, rates and covid to inflation, rates and Ukraine.

Overview

Just as the global economy was saying goodbye to the COVID-19 pandemic, the world faces another shock from Russia’s invasion of Ukraine. Unprecedented sanctions have been placed on the Russian economy by Western governments and Russian stocks have been dropped from global index providers and by most managed funds. Oil, European gas prices, nickel and wheat all surged in response to the conflict and drove higher commodity prices more generally.

More than a glimmer of hope has been provided by Ukraine’s strong resistance and the roll back of Russian armed forces from Kiev at the time of writing. Partly in response, market performances were stronger in the month of March than over the quarter as a whole. While these are uncertain times, Russia and Ukraine are not large contributors to the global economy outside of the commodity markets mentioned above, and history suggests that recovery from small scale conflicts is rapid. That said, the war has clearly raised global inflation and inflationary risks at a time when central banks were already “behind the curve” in terms of getting on top of surging inflation rates.

Market performances over the quarter were very much driven by the contrasting impacts of the conflict. Most equity markets fell, as did bonds as higher inflation and interest rate risks were priced in. Within equities, resource stocks rallied strongly, benefitting the Australian equity market with its large mining and energy sector.

Asset classes expected to be more resilient to inflation risks, such as infrastructure, property and gold, were also relatively resilient.

Market Roundup

Developed market equities fell around 6.5% over the March quarter in NZD terms while NZD hedged equities fell around 5%. While a poor result, it is on the back of very strong returns in 2021, with the annual return to March 2022 being around 11%. Within global equities, higher risk small caps had a much weaker annual return (-0.5%) while value stocks have out-performed as the shine has come off growth-oriented stocks towards companies with lower valuations, and hence less reliance on future growth conditions.

Emerging Market (EM) equities bore the brunt of the sell off as war broke out in Ukraine, falling around 8.5% in the quarter and 11% over the year to March 2022. It is important to note that the contribution of Russian stocks to this fall was modest given Russian equities were only a small part of emerging market indexes. In response to the invasion and sanctions placed on Russia, EM index providers have removed it from their indexes and fund managers have followed suit.

NZ and Australian equity market performances were very mixed.

Australian stocks increased around 4% over the quarter, driven by a huge rally in its resources sector (up over 20%). New Zealand equities fell around 3% as the RBNZ increased interest rates and as risk appetites waned.

International infrastructure and property stocks had a relatively strong quarter as they are generally resilient to a higher inflation environment. International property stocks fell around 3% in the quarter but returned 16% over the year.

Global infrastructure stocks – as we feature below – returned around 2.5% in the quarter and 18% over the year. As shown in the graph on page 4 these are stand out performances over the year.

On the flip-side, bonds are less resilient to rising inflation and interest rates.

As a consequence, New Zealand and offshore investment grade (IG) bonds with benchmark terms (or duration) both fell around 4% in the quarter and have similarly sized negative returns over the year. In contrast, bonds with short terms and ‘cash enhanced’ exposures, to which we have tilted portfolios given our concern over inflation risks, fared much better and eked out small positive returns.

Infrastructure and the role it has in your portfolio

The portfolios we offer have around a 5% weight to global listed infrastructure. Infrastructure assets provide essential services for societies to function and consist of physical assets that are costly and difficult to replace. Examples include electricity transmission, water utilities, air and seaports and various cellular networks and data centres.

The inclusion of infrastructure in portfolios is motivated by several factors.

First, many infrastructure companies have monopolistic functions in the market, which enables them to have true pricing power. As a result, this asset class is often seen as one of the best ways to protect against rising inflation.

Second, the long-dated nature of the assets and essential services they tend to offer provides stable and repeatable earnings, which are resilient through a market cycle. That is, the asset class tends to be a ‘defensive’ growth asset which normally outperforms in a market sell-off – as occurred over the March quarter.

Third, infrastructure stocks (like listed property stocks) tend to have higher dividend yields than equities overall. Given these features, infrastructure is likely to offer a portfolio diversification benefit.

Portfolio allocations

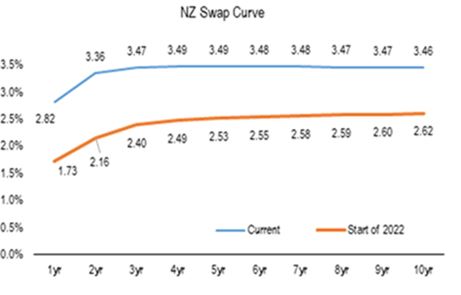

We continue to be broadly comfortable with the portfolio allocations following large changes we made within fixed income in 2021. However, as illustrated by Forsyth Barr in Figure 1 interest rates in New Zealand are now well above where they were at the beginning of the year.

As a result, NZ bonds are now approaching our estimated fair value when we would start to reduce the large underweight to benchmark duration fixed income. Global bonds are further from our fair value estimates and so we do not propose changing our short duration positioning yet.

Figure 1: The NZ Swap Curve is well above where it was at the beginning of the year

Disclosure

The information contained in this report is given in good faith and has been derived from sources believed to be accurate. However, neither IWIinvestor (Taupō Moana Investments Limited) nor its associated companies nor any of their employees or directors gives any warranty of reliability or accuracy nor accepts any responsibility arising in any other way for errors or omissions.